Sequence of Returns Risk

Most people have heard that “the market averages about 7% per year.” While that statement is generally true over long periods of time, it leaves out one critical factor that becomes especially important in retirement: the sequence of returns. The order in which gains and losses occur does not matter nearly as much during the accumulation years—but it can make all the difference once a client begins withdrawing income.

During the working years, clients operate under one set of rules. They are earning income, contributing to retirement accounts, often receiving employer matches, and—most importantly—NOT withdrawing funds. They have time on their side. When markets decline, as they did in 2008 when many portfolios dropped around 40%, those losses can eventually recover.

Why? Because clients continue contributing, continue receiving matches, and benefit from the most powerful force in investing: TIME. Over almost 20 years since the financial crisis, portfolios not only recovered but often grew significantly higher due to compounding and consistent contributions.

Time is the greatest compounder of money. During the accumulation phase, investors can afford volatility because time is working in their favor.

However, the rules change in retirement. Around age 65, clients typically stop working, stop contributing, stop receiving employer matches, and begin withdrawing income from their portfolios. Now, time is no longer an ally in the same way. If a market downturn occurs early in retirement while withdrawals are being taken, the portfolio can suffer what is known as sequence of returns risk. Even if the long-term average return remains around 6–7%, the order of those returns can dramatically impact sustainability.

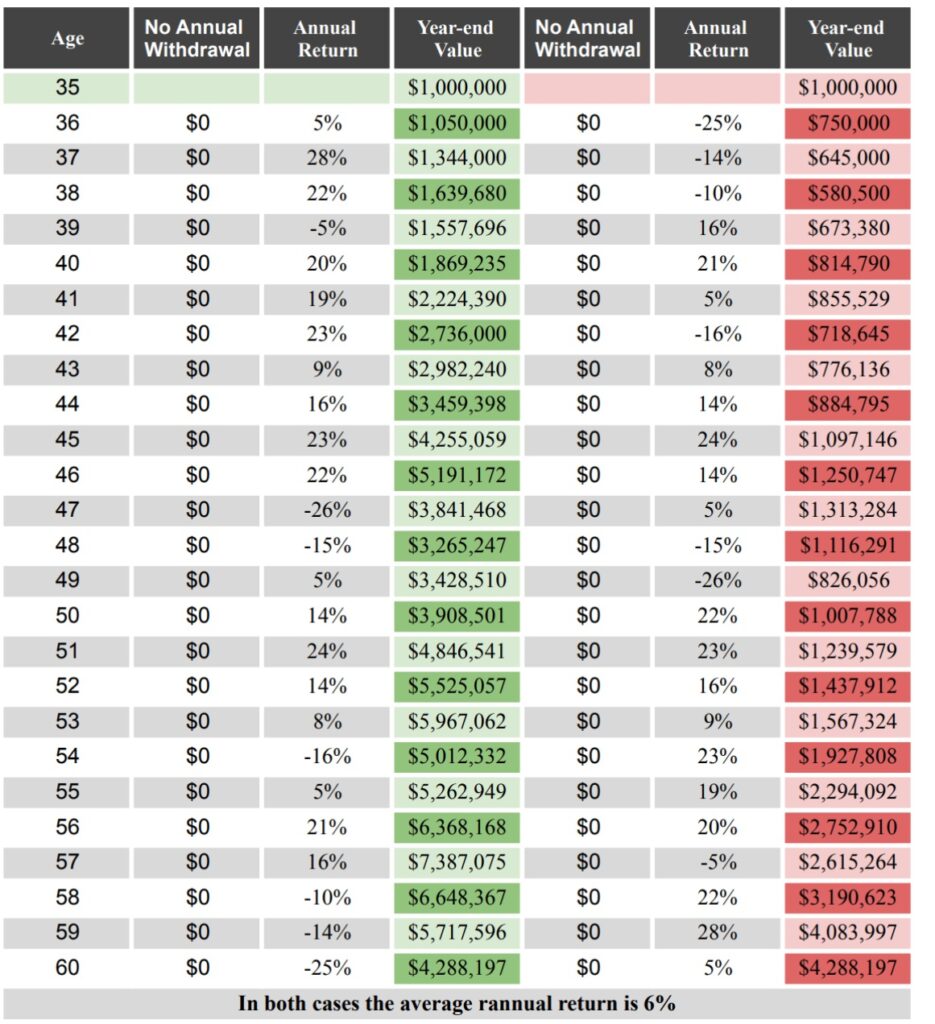

For example, consider two portfolios with the exact same annual returns, simply in reverse order. The green & red column on the left both start with 1 million and both end with 4,288,197. They average 6% returns. Again, they are the exact same returns just flipped.

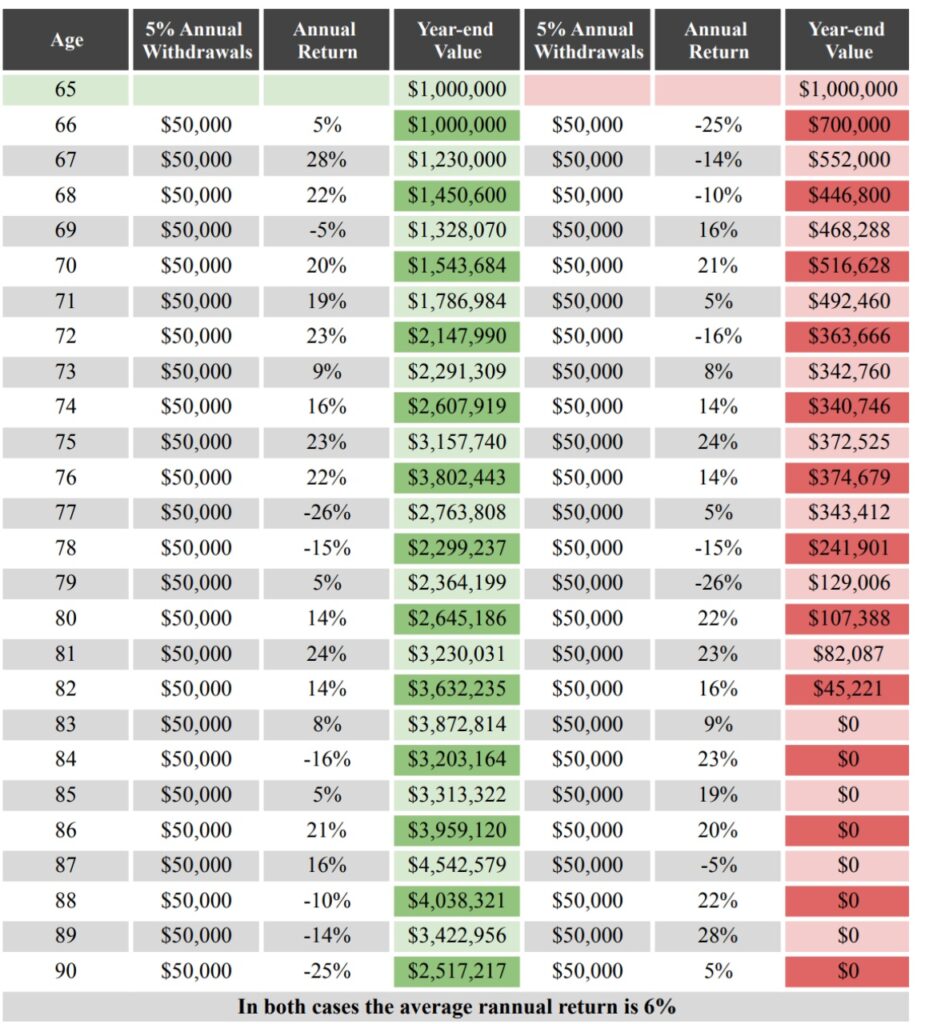

It does not make a difference when you are NOT withdrawing funds. However, once retired and you start accessing the funds you have worked so hard to put away and save. Now, the outcome changes significantly. See what happens on the right, when you start withdrawing $50,000/year.

If positive returns occur in the early years of retirement, the portfolio may remain stable and sustainable. But if negative returns occur early while withdrawals continue, the portfolio experiences a double compounding effect: losses reduce principal, and withdrawals lock those losses in place. This can accelerate depletion and increase the likelihood of running out of money.

This is why annuities and other protected income strategies play a critical role in retirement planning. They are not designed to “beat the market.” Instead, they are designed to address risks that the market does not solve—specifically longevity risk and sequence of returns risk. By creating a reliable income floor that is not directly exposed to market downturns, agents can help clients shift from accumulation rules to retirement rules with greater confidence and stability.

Understanding that the rules change at retirement is essential. The average return is only part of the story. The timing of returns—and the presence of withdrawals—can determine whether a client’s money lasts a lifetime.