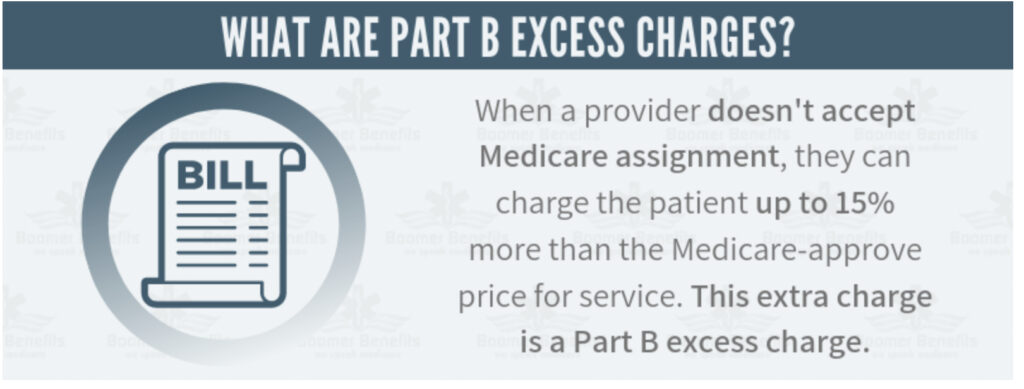

When you visit a doctor or specialist under Medicare, they agree to accept the Medicare-approved amount for services as full payment. However, not all doctors accept this.

Doctors who do not accept Medicare “assignment” can legally charge up to 15% more than the Medicare-approved amount.

This additional cost is known as a Part B Excess Charge.

Example:

Medicare approves $100 for a service.

A non-participating doctor can charge $115.

You are responsible for that extra $15, which is the excess charge.

Why Part B Excess Charges Matter

These charges:

Are not common, but can happen, especially with specialists.

Are unpredictable and can add up quickly for clients who see doctors regularly.

Can cause confusion and frustration for clients who don’t understand why they’re being billed unexpectedly.

From a customer service standpoint, these calls are avoidable with proper education upfront.

How Medigap Plans Handle Excess Charges

How Medigap Plans Handle Excess Charges

| Medigap Plan | Covers Excess Charges? |

|---|---|

| Plan F |  Yes Yes |

| Plan G | Yes |

| Plan N |  No No |

| Other Plans | Usually No |

Plan F and Plan G fully cover Part B Excess Charges. If a doctor charges more than Medicare allows, your client won’t pay a cent of the excess.

Plan N does not cover excess charges. If a doctor charges more than Medicare allows, your client pays the difference.

What Else to Know About Plan N

In addition to not covering excess charges, Plan N out of pocket charges includes:

Must pay the Part B deductible (just like Plan G)

$20 copay for doctor visits

$50 copay for urgent care

So while Plan N has lower premiums, the out-of-pocket costs can be higher and less predictable.

How to Talk to Clients About Plan N

Agents and clients are often drawn to Plan N because of its lower monthly premium, and that’s understandable. But clients must be aware of the trade-offs:

Plan N is a viable, affordable choice for many.

However, if the client visits the doctor frequently or sees specialists who charge excess fees, those small savings on the premium can quickly disappear.

If they’re hit with unexpected bills, it can lead to irritation, mistrust, and service issues—something both you and the client want to avoid.

Best Practices for Agents

Explain what excess charges are and that Plan N does not cover them.

If cost savings is the top priority and the client is healthy and doesn’t see doctors often, Plan N might be a good fit.

If the client wants peace of mind and predictability, Plan G (or F, if eligible) may be better.

Key Takeaways

Part B Excess Charges are legal but not always charged.

Plan F and G protect clients from excess charges.

Plan N does not—and also includes copays and deductible.

Client education upfront avoids surprises, complaints, and service headaches later.